Abstract

This article analyzes in depth the impact of global temperature variations on inflation in Gabon through the application of an Autoregressive Distributed Lag (ARDL) model. The analysis is based on annual data covering the period 1990–2023, which makes it possible to capture both the short- and long-term dynamics between climate shocks and price fluctuations. The central objective is to understand how climate anomalies, particularly temperature increases, translate into macroeconomic instability in a country that is highly dependent on imports and whose infrastructure remains vulnerable to external shocks. The results show that a one-degree Celsius rise in average global temperature compared to the 20th-century baseline leads to a long-term increase of approximately 94 points in the Consumer Price Index (CPI). This reflects not only higher prices for essential goods but also a deterioration in the monetary well-being of households, especially the most fragile groups. In the short run, climate shocks tend to generate immediate inflationary pressures, often followed by temporary deflationary episodes as markets attempt to adjust. These fluctuations are amplified by structural weaknesses, such as heavy reliance on imported food products, limited diversification of the economy, and insufficient resilience of transport and energy systems. By integrating climate dynamics into inflation analysis, this study fills a gap in the African economic literature, where environmental variables are still rarely included in macroeconomic models. The findings provide useful insights for policymakers by emphasizing the urgent need for climate adaptation strategies, economic diversification, and stronger social protection systems. In doing so, the paper contributes to the broader debate on the links between climate change, price stability, and sustainable development in Sub-Saharan Africa, using Gabon as a case study.

Keywords

Gabon, Climate, Temperature Anomaly, ARDL, Inflation, CPI

1. Introduction

Climate change is now a major global issue, affecting not only ecosystems but also economies worldwide. Among its various impacts, inflation—resulting directly from climate-related disruptions—raises particular concerns in developing countries such as Gabon. The rise in global temperatures, combined with climate anomalies, influences the prices of goods and services, mainly by disrupting supply chains, agricultural systems, and energy markets. In Gabon, where the economy heavily relies on the importation of essential goods and vulnerable infrastructures, these dynamics can exacerbate inflationary pressures and impact household well-being.

Despite increasing recognition of the effects of global warming on economic dynamics, specific research on the relationship between rising temperatures and inflation in the Gabonese context remains scarce. This gap limits the understanding of the mechanisms through which climate influences prices in a country particularly exposed to climate variability. This raises a crucial question: To what extent do global temperature changes influence inflation in Gabon?

This study aims to analyze the impact of global temperature variations on inflation in Gabon using an Auto-Regressive Distributed Lag (ARDL) model. More specifically, it seeks to examine the short- and long-term effects of climate anomalies on the Consumer Price Index (CPI) while considering explanatory variables such as GDP per capita, unemployment rate, and urbanization level.

The methodological framework is based on time-series data covering the period 1990–2023, with the CPI as the dependent variable and temperature anomalies as the primary explanatory variable. The ARDL methodology is employed due to its ability to model dynamic relationships between variables with different orders of integration while providing reliable short- and long-term impact estimates.

This research contributes to the existing literature by focusing on Gabon, a country rarely studied in economic analyses related to climate change. It offers an innovative approach by integrating climate dynamics into the study of inflation, moving beyond traditional monetary or cost-based analytical frameworks. The findings also provide valuable insights for policymakers aiming to mitigate the effects of climate change on household well-being.

The article is structured as follows: a literature review explores the links between global warming and inflation; the methodology and data are detailed in the next section; empirical results are then presented, followed by an in-depth discussion and a conclusion offering recommendations tailored to the Gabonese context.

2. Literature Review

Climate change has both direct and indirect repercussions on global economies, particularly affecting climate-sensitive sectors such as agriculture and energy.

| [14] | Stern, N., et Taylor, C. (2007). Changement climatique: risque, éthique et la revue Stern. Science, 317 (5835), 203-204. |

[14]

highlighted that extreme weather events, such as droughts and floods, disrupt supply chains, thereby contributing to inflationary pressures. These impacts materialize through several mechanisms, notably in food prices, energy costs, and financial markets.

Climate anomalies, by disrupting agricultural systems, increase production costs, leading to food inflation, which is particularly severe in developing countries where the primary sector plays a crucial role

| [4] | Burke, M., Hsiang, S. M. et Miguel, E. (2015). Effet non linéaire global de la température sur la production économique. Nature, 527(7577), 235-239. |

| [12] | Ramesh, Allipour, Birgani., Ali, Kianirad., Sakineh, Shab-Bidar., Abolghasem, Djazayeri., Hamed, Pouraram., Amirhossein, Takian. (2022). 4. Climate Change and Food Price: A Systematic Review and Meta-Analysis of Observational Studies, 1990-2021. American Journal of Climate Change, https://doi.org/10.4236/ajcc.2022.112006 |

[4, 12]

. Rising temperatures contribute directly to this trend, with projections anticipating a global annual inflation increase of 0.92 to 3.23 percentage points by 2035

| [9] | Maximilian, Kotz., Friderike, Kuik., Eliza, Lis., Christiane, Nickel. (2023). 2. The Impact of Global Warming on Inflation: Averages, Seasonality and Extremes. Social Science Research Network, https://doi.org/10.2139/ssrn.4457821 |

| [8] | Maximilian, Kotz., Friderike, Kuik., Eliza, Lis., Christiane, Nickel. (2024). 1. Global warming and heat extremes to enhance inflationary pressures. https://doi.org/10.1038/s43247-023-01173-x |

[9, 8]

. A study by

| [7] | Hyacinth, E., Ichoku., Ihuoma, Anthony., Tosin, Olushola., Apinran, Martins. (2023). 5. Modelling Dynamic Linkage between Climate Change and Food Inflation in Nigeria. International Journal of Enviornment and Climate Change, https://doi.org/10.9734/ijecc/2023/v13i113272 |

[7]

also revealed that climate shocks significantly raise food prices in Nigeria, underscoring the need for adaptive agricultural practices to mitigate these challenges. Furthermore, extreme weather events such as droughts intensify these pressures, with

| [17] | Birgani, RA, Kianirad, A., Shab-Bidar, S., Djazayeri, A., Pouraram, H., et Takian, A. (2022). Changement climatique et prix des denrées alimentaires: revue systématique et méta-analyse d’études observationnelles, 1990-2021. American Journal of Climate Change, 11 (2), 103-132. |

[17]

estimating that food prices could rise by up to 32% under such conditions.

Climate change also influences energy markets, increasing demand for heating and cooling, thereby exacerbating price volatility.

| [5] | Dell, M., Jones, B. F., & Olken, B. A. (2012). Temperature shocks and economic growth: Evidence from the last half century. American Economic Journal: Macroeconomics, 4(3), 66-95. |

[5]

demonstrated a direct link between high temperatures and fluctuations in energy prices. Additionally, climate policy uncertainties (CPU) and carbon emissions (CO₂) have major repercussions on natural gas and oil markets

| [2] | Amar, Rao., Brian, Lucey., Satish, Kumar. (2023). 1. Climate risk and carbon emissions: Examining their impact on key energy markets through asymmetric spillovers. Energy Economics, https://doi.org/10.1016/j.eneco.2023.106970 |

[2]

.

highlighted that fossil fuel price volatility surged significantly after the global financial crisis, reinforcing the notion of a strong correlation between climate factors and energy market fluctuations.

At the same time, financial markets are not immune to these effects.

| [3] | Batten, S., Sowerbutts, R. et Tanaka, M. (2020). Changement climatique: impact macroéconomique et implications pour la politique monétaire. Les risques écologiques, sociétaux et technologiques et le secteur financier, 13-38. |

[3]

emphasized the impact of climate risks on risk premiums and interest rates, further amplifying long-term inflationary pressures.

| [15] | Yang, X., Xiong, J., Du, T., Ju, X., Gan, Y., Li, S.,... & Butterbach-Bahl, K. (2024). La diversification de la rotation des cultures augmente la production alimentaire, réduit les émissions nettes de gaz à effet de serre et améliore la santé des sols. Nature Communications, 15 (1), 198. |

[15]

demonstrated a positive correlation between CO₂ emissions and stock market returns, reflecting investor expectations for higher returns as compensation for climate-related risks.

However, these effects vary across regions and sectors. Developing countries, due to their reliance on food and energy imports, are particularly vulnerable to climate-induced inflation

| [6] | Fonds Monétaire International (FMI) (2021). World Economic Outlook: Managing Divergent Recoveries. FMI Publications. |

[6]

. Their limited financial resources make adaptation more challenging, in contrast to developed nations, which—despite being indirectly affected by global supply chain disruptions—have more robust mitigation capacities

| [11] | Paul, Chinowsky., Carolyn, Hayles., Amy, Schweikert., Niko, Strzepek., Kenneth, Strzepek., C., Adam, Schlosser. (2011). 1. Climate change: comparative impact on developing and developed countries. https://doi.org/10.1080/21573727.2010.549608 |

| [1] | Alla, Semenova. (2023). 2. Rising temperatures and rising prices: the inflationary impacts of climate change and the need for degrowth-based solutions to the ecological crisis. Globalizations, https://doi.org/10.1080/14747731.2023.2222482 |

[11, 1]

. Finally, while the agricultural sector remains the most exposed, manufacturing and services industries are also significantly impacted, as revealed by the findings of

| [16] | Khan, Z., Badeeb, RA, et Nawaz, K. (2022). Ressources naturelles et performance économique: évaluation du rôle du risque politique et de la consommation d’énergies renouvelables. Politique des ressources, 78, 102890. |

[16]

.

3. Methodology

This section presents the data sources, econometric techniques, and the methodological steps adopted to analyze the impact of climate change on inflation.

We adopt a new approach to inflation, moving away from traditional theories such as those of Friedman (who argued that "inflation is always and everywhere a monetary phenomenon"), Keynesian theories, and cost-push or import-driven inflation models. Instead, we examine inflation through the lens of climate change dynamics. Our research hypothesis, which we will test, is whether climate change—captured through global warming—leads to higher inflation levels in Gabon.

The data used to test our hypothesis are primarily sourced from the World Bank and Statista (for temperature anomalies), covering the period 1990 to 2023.

1. Dependent variable: The Consumer Price Index (CPI), which measures the evolution of average prices of goods and services consumed by households, reflecting the cost of living. CPI is often preferred over general inflation measures as it provides a precise and tangible indicator of price variations affecting consumers directly.

2. Main explanatory variable: Temperature anomaly, a key measure of global warming, defined as the difference between an observed temperature and a reference average over a given period (here, the 20th-century average). Measured in degrees Celsius, temperature anomalies highlight deviations from normal conditions, making them useful for tracking global and local warming or cooling trends independently of seasonal or local fluctuations.

3. Control variables:

a. Unemployment rate

b. Urbanization rate

c. GDP per capita (GDP/capita)

To model our hypothesis, we use an Auto-Regressive Distributed Lag (ARDL) model, which is well-suited for analyzing the impact of climate change on inflation. The ARDL model is advantageous because:

1. It captures both short-term and long-term dynamics between variables.

2. It accommodates variables with different integration orders (I(0) or I(1)), making it flexible for time-series analysis.

3. It allows for cointegration testing (long-term equilibrium relationships) and provides robust long-term coefficient estimates, even with small sample sizes.

4. It facilitates the inclusion of control variables (GDP/capita, unemployment, urbanization rate) for a comprehensive analysis.

5. It offers clear interpretations of both immediate and lagged effects of temperature anomalies on inflation.

The functional form of our equation will be:

And its mathematical form:

It should be noted that the terms capture the short-term variations of the dependent and explanatory variables, while represent the long-term relationship between the variables, and the error term accounts for unexplained shocks.

------ Measurement of short-term effects

------ Measurement of long-term effects

It should also be noted that we did not take logarithms, likely to avoid interpretation issues and negative values, particularly for the temperature anomaly. Moreover, some variables, such as urbanization, are already stationary in levels, making a logarithmic transformation unnecessary. The absence of logarithms also allows for a direct interpretation of the coefficients in absolute variations. Finally, in the context of Gabon, where economic variables fluctuate significantly, the level model better captures these dynamics.

Estimation Procedure

Table 1. Steps for Estimating the ARDL Model.

Step 1 | Stationarity Tests |

Step 2 | Cointegration Test |

Step 3 | Model Estimation |

Step 4 | Residual Autocorrelation Tests |

Step 5 | Heteroscedasticity Test |

Step 6 | Normality Test |

Step 7 | Stability Test |

Source: Authors.

The estimations of our model will be conducted using STATA, specifically version 17. Notably, in STATA, the best model is automatically selected by minimizing criteria such as AIC, HQIC, and FPE when modeling ARDL. As a result, the step of determining the optimal lag structure is no longer necessary.

4. Results

Stationarity Tests

A stationarity test is used to determine whether a time series is stationary, meaning that its statistical properties (mean, variance, and autocorrelation) remain constant over time. In ARDL modeling, stationarity is crucial because this method assumes that variables are either stationary (I(0)) or integrated of order 1 (I(1)), but not of a higher order (I(2)). The stationarity test ensures that the necessary conditions for using an ARDL model are met. The most commonly used tests in this context are the Augmented Dickey-Fuller (ADF) test, the Phillips-Perron (PP) test, and the KPSS test. These tests help determine whether a series requires differencing before being included in the ARDL model, ensuring valid and reliable econometric results.

Table 2. Results of Phillips-Perron (PP) and Augmented Dickey-Fuller (ADF) Stationarity Tests.

| Phillips-perron (PP) test | Dickey-Fuller Augmenté (ADF) test |

Level | First Difference | Level | First Difference | Decision |

| 0.9825 | 0.0001*** | 0.9804 | 0.0001*** | |

| 0.9688 | 0.0000*** | 0.8641 | 0.0000*** | |

| 0.0000*** | | 0.0000*** | | |

| 0.7537 | 0.0019*** | 0.8063 | 0.0017*** | |

| 0.6664 | 0.0000*** | 0.6568 | 0.0000*** | |

Source: Authors, based on Stata 17 software.

Cointegration Test

A cointegration test verifies the existence of a long-term equilibrium relationship between non-stationary variables. It is crucial to avoid spurious regressions in time series analysis. The main tests include Engle-Granger, Johansen, and the Bounds test by Pesaran et al. (2001). In ARDL modeling, the Bounds test is particularly suitable, as it is effective when variables have mixed integration orders (I(0) or I(1)). This test helps determine whether a cointegration relationship exists, even with a small sample. The key importance of cointegration testing lies in ensuring that the estimated relationships genuinely reflect long-term economic dynamics. In the ARDL framework, the Bounds test is recommended for its flexibility and ability to handle dynamic relationships in time series data.

Table 3. Critical Value Results for the ARDL Bounds Test by Pesaran, Shin, and Smith (2001).

Statistic | Coefficient | I(0) L_1 | I(1) L_1 | I(0) L_05 | I(1) L_05 | I(0) L_025 | I(1) L_025 | I(0) L_01 | I(1) L_01 |

F | 5.922 | 2.45 | 3.52 | 2.86 | 4.01 | 3.25 | 4.49 | 3.74 | 5.06 |

T | -2.329 | -2.57 | -3.66 | -2.86 | -3.99 | -3.13 | -4.26 | -3.43 | -4.60 |

I(0) and I(1) represent the non-deterministic regressors in the long-term relationship. L_1, L_05, L_025, and L_01 denote the significance levels (1%, 2.5%, 5%, and 10%). K = 4 refers to the number of non-deterministic regressors in the long-term relationship.

Source: Authors, based on Stata 17 software.

Interpretations: Here, the F-statistic (5.922) is higher than the upper critical bound (I_1) at all conventional significance levels, allowing us to reject the null hypothesis of no long-term relationship. Moreover, the t-statistic (-2.329) falls within the associated critical intervals, further supporting the presence of a stable link between the variables. These results therefore suggest a significant long-term relationship between the model’s variables.

Model Estimation

Table 4. ARDL Model Estimation Results.

Long term |

Variables | Coefficients | Probabilities |

| | *** |

| | *** |

| | ** |

| | * |

Short term |

Variables | Coefficients | Probabilities |

| | *** |

| | 0.000*** |

| | 0.000*** |

| | 0.000*** |

| | 0.000*** |

| | 0.137 |

| | 0.000*** |

| | 0.000*** |

| | |

| | |

Interpretation of the ARDL Model

The ARDL(1,2,0,2,0) model examines the relationships between the Consumer Price Index (CPI) and the explanatory variables: temperature anomaly, GDP per capita (GDP/capita), urbanization, and unemployment, using a sample of 31 observations (1993–2023). The model has an R-squared of 0.9163, indicating that 91.63% of the variability in CPI is explained by the model, with an adjusted R-squared of 0.8805, reflecting a good overall fit. The long-term equilibrium adjustment term, represented by L1.CPI, has a coefficient of -0.2155 (p = 0.030), indicating an error correction mechanism where 21.55% of deviations are corrected each period, suggesting a gradual but slow return to equilibrium.

The long-term effects show that the temperature anomaly (L1) has a significant coefficient of 94.1147 (p = 0.026), implying that a one-unit increase in the temperature anomaly raises the CPI by 94.11 in the long run. GDP per capita (L1) has a slightly positive effect (0.004978, p = 0.061), while urbanization (L1) reduces CPI by 7.7543 (p = 0.024), suggesting economic gains associated with urbanization (e.g., mass innovation). Unemployment (L1) has an inflationary effect, increasing the CPI by 3.5031 (p = 0.049) for every 1% increase in the unemployment rate.

The short-term effects reveal interesting dynamics. The temperature anomaly has an immediate inflationary effect (D1 = 14.9409, p = 0.000), followed by a delayed deflationary adjustment (LD = -13.5678, p = 0.000). GDP per capita (D1) has a weak but significant immediate effect on CPI (0.001073, p = 0.000). Urbanization (D1) has a strong immediate deflationary effect (-76.2365, p = 0.000), which is partially offset by a delayed inflationary effect (LD = 41.4590, p = 0.000). In contrast, the immediate effect of unemployment (D1) is not significant (0.7551, p = 0.137). The constant (_cons) is significant (147.2055, p = 0.000), indicating a baseline CPI trend in the absence of variations in explanatory variables.

Post-Estimation Analysis

Residual Autocorrelation Test

A serial autocorrelation test detects correlation between the residuals of an econometric model at different time lags. Autocorrelation violates the fundamental assumption of error independence, which is essential to ensure the statistical validity and efficiency of the estimates. In Auto-Regressive Distributed Lag (ARDL) models, these tests are particularly important because ARDL relies on complex interactions between lagged variables. Autocorrelated residuals may indicate a model misspecification, such as an insufficient number of lags or the omission of a key variable. Uncorrected autocorrelation can also bias the results of cointegration tests or affect the reliability of short- and long-term coefficient estimates. Several tests are used for this purpose: the Durbin-Watson test (simple but limited for models with lagged variables), the Breusch-Godfrey test (which detects higher-order autocorrelations), the Ljung-Box test (or Portmanteau test) (which checks for overall autocorrelation), and the LM test of Breusch-Godfrey (specific to time series). These tests help validate ARDL model specification, ensuring robust and reliable estimates.

Thus, for our model, we will use the Breusch-Godfrey LM test:

Table 5. Results of the Breusch-Godfrey Autocorrelation Test of Order 1.

| | | |

| | | |

Source: Authors, based on Stata 17 software.

Interpretation: The Breusch-Godfrey test checks for the presence of residual autocorrelation. Here, with a p-value = 0.4684 (greater than 5%), we do not reject the null hypothesis (H0) of no autocorrelation. This indicates that the residuals do not exhibit significant serial correlation, confirming the validity of this assumption in the estimated model.

Heteroscedasticity Test

A heteroscedasticity test in econometrics assesses whether the variance of a model’s residual errors is constant or not. The fundamental assumption of Ordinary Least Squares (OLS) is that residual variance remains constant, a condition known as homoscedasticity. When this assumption is violated, heteroscedasticity occurs, leading to biased standard errors, unreliable significance tests for coefficients, and incorrect confidence intervals. In ARDL models, where dynamic interactions between variables are crucial, heteroscedasticity can distort the interpretation of both short- and long-term relationships. Several tests are commonly used to detect this issue: the Breusch-Pagan test, which examines whether the variance of errors depends linearly on explanatory variables; the White test, a more general test that does not assume a specific form of heteroscedasticity; and the Glejser test, which detects direct relationships between the absolute values of residuals and independent variables. Identifying and correcting heteroscedasticity is essential to ensure robust estimates and valid inferences in econometric models. This can be achieved by adjusting standard errors using robust methods such as White’s or Newey-West’s correction. Thus, in our study, we have chosen the White test.

Table 6. White Heteroscedasticity Test.

Variable | Chi2 | Probability |

| | |

Source: Authors, based on Stata 17 software.

Interpretation: The White test examines the hypothesis of homoscedasticity. With a p-value = 0.4154, we do not reject the null hypothesis of homoscedasticity, indicating that the model's residuals do not exhibit non-constant variance. The Cameron & Trivedi decomposition also confirms the absence of significant issues related to heteroscedasticity, skewness, or kurtosis in the data.

Normality Test

A normality test in econometrics assesses whether the residuals of a model follow a normal distribution, which is a key assumption of Ordinary Least Squares (OLS). Residual normality is essential to ensure the validity of significance tests, confidence intervals, and predictions. In ARDL models, where short- and long-term estimates rely on strong assumptions, non-normal residuals may indicate model misspecification or the presence of outliers. Several tests are commonly used to verify this assumption: the Jarque-Bera test, which examines the skewness and kurtosis of residuals; the Shapiro-Wilk test, particularly effective for small samples; and the Kolmogorov-Smirnov test, which compares the residual distribution to a normal distribution. If normality is violated, variable transformations or robust methods, such as bootstrap techniques, can be used to ensure reliable inferences. Testing residual normality is therefore a crucial step in validating the relevance and robustness of econometric results.

We have chosen the Kolmogorov-Smirnov test.

Table 7. Result of the Kolmogorov-Smirnov Residual Normality Test.

Variable | D | Probability |

| | |

| | |

| 0.0849 | 0.975 |

Source: Authors, based on Stata 17 software.

Interpretation: The Kolmogorov-Smirnov test shows that the residuals of our model do not significantly differ from a normal distribution (D = 0.0835, p = 0.640). The high p-values for all tests (residuals, cumulative, and combined) indicate that the normality assumption of the residuals is met. Therefore, we can consider our residuals to be normally distributed, which validates this key assumption for statistical inference.

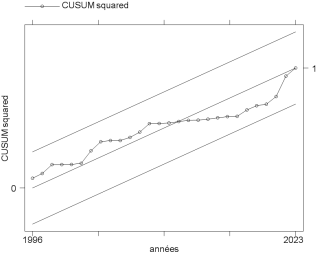

Stability test

A stability test of the model evaluates the robustness of the estimated relationships by verifying whether the parameters (coefficients) remain constant throughout the study period. In an ARDL model, these tests are particularly important as they ensure that the short- and long-term relationships between variables are reliable. Several tests exist: the CUSUM test, which checks whether cumulative residuals remain stable; the CUSUMSQ test, which detects variations in the residual variance; structural break tests such as Chow’s test or Bai-Perron’s test, which identify changes in relationships between variables; and graphical analyses of coefficients. These tests are crucial in an ARDL model for several reasons. First, they ensure the validity of long-term relationships, which rely on the assumption of parameter stability. Second, they detect structural breaks caused by events such as climate shocks, oil shocks, or economic crises, which are common in countries like Gabon. Third, they ensure that the model produces reliable forecasts by avoiding biases due to unstable economic relationships. Finally, they validate econometric diagnostics and ensure that the results accurately reflect underlying economic dynamics. In summary, stability tests are essential to guarantee the robustness of conclusions and the relevance of recommendations based on an ARDL model.

For the stability test, we chose to perform the CUSUMQ test, and the relationship appears to be stable.

Potential Omitted Variable Issues:

Although other factors, such as money supply, exchange rate, and commodity prices, may influence inflation, our model focuses on internal structural and economic determinants. Monetary and external effects are partially captured by the included variables, and robustness tests—including autocorrelation, heteroscedasticity, and normality of errors—indicate that omitting these variables does not significantly affect the model's validity. Furthermore, the absence of error variance issues reinforces the credibility of the chosen specification. Therefore, their inclusion is not essential within our analytical framework.

5. Discussions

Short-Term Analysis of the Relationship Between Climate Change and Inflation

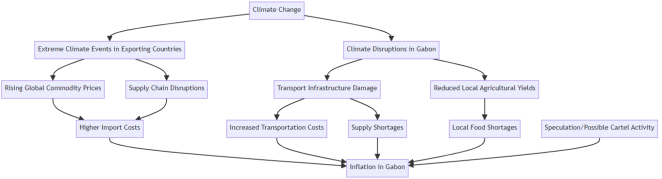

The results show an immediate inflationary effect of temperature anomalies, followed by a later deflationary adjustment.

Immediate Inflationary Effect in the Short Term

This immediate effect can be explained by several dynamics specific to the Gabonese economy, which is highly dependent on external factors and vulnerable to climate disruptions. Gabon imports a significant share of the goods it consumes, particularly food and manufactured products. When exporting countries experience extreme climate events (such as droughts or heavy rains), global commodity prices rise, directly impacting Gabonese consumers due to the country's high dependence on external supply. Additionally, temperature anomalies can disrupt international supply chains, a recurring issue in developing countries. These disruptions delay or limit access to essential goods, further intensifying price increases. For instance, a drought in a cereal- or vegetable oil-producing country would lead to higher prices on the Gabonese market, exacerbating inflation.

In Gabon, transport infrastructure is particularly vulnerable to climate disruptions. Climate change effects such as torrential rains or landslides can paralyze roads, ports, and railways. A striking example is the landslide that destroyed over 900 meters of railway tracks on the Transgabonais in December 2022

. This railway is a critical supply route for five provinces and, indirectly, the entire country. Such disruptions cause delays and supply shortages, increasing transportation costs and, consequently, the prices of goods nationwide.

Although Gabon’s agriculture remains underdeveloped compared to its potential, it is still crucial for rural populations and urban market supplies. A climate anomaly, such as prolonged droughts or excessive rainfall, can significantly reduce agricultural yields for staple products like cassava, bananas, and palm oil. This is evident in rising cassava prices, which directly impact purchasing power, as well as increases in banana prices and other locally produced goods. These local shortages lead to food price surges, disproportionately affecting low-income households.

Speculation by certain economic actors, particularly wholesalers and major retailers (noting that today, there is a perceived possibility of a cartel-like arrangement among them), also plays a role in the immediate inflationary effect. These actors may exploit climate disruptions to artificially raise prices, citing supply difficulties as justification. Such practices worsen inflationary pressures, creating a vicious cycle where prices continue to rise even in the absence of actual shortages.

Figure 2. Summary of immediate short-term inflationary effect.

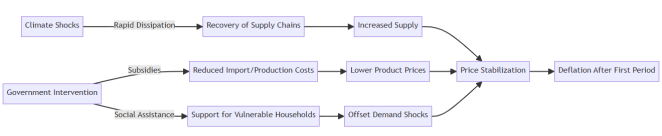

Non-immediate short-term deflationary effect

One hypothesis explaining the deflation after the first period could be the rapid dissipation of climate shocks, both nationally and internationally. The absence of prolonged disruptions would allow for a gradual adjustment in production, a recovery of supply chains, and an increase in supply, which would stabilize prices. Another possible hypothesis is the role of subsidies on product prices, whether for imports or local production. These subsidies, along with social aid programs, which are particularly common in Gabon, could help reduce inflationary pressure. Indeed, although social aid generally tends to stimulate demand, its precise targeting can have a stabilizing effect during crises by offsetting the shocks experienced by the most vulnerable households.

These mechanisms are largely financed by oil revenues, which increase during periods of high global energy demand. This increased demand can be driven by extreme climate events requiring more energy (heating, air conditioning, emergency response), although this contradicts global efforts toward energy transition. Nevertheless, Gabon's dependence on oil revenues highlights the importance of diversifying its economy to sustain such policies in the face of fluctuating oil prices.

Figure 3. Summary of Non-immediate short-term deflationary effect.

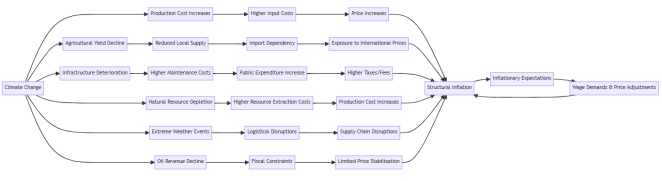

Long-term analysis of the relationship between climate change and inflation.

In the long run, global warming profoundly transforms Gabon's economic structures, leading to sustained inflation through structural and systemic mechanisms. Frequent climate disruptions increase production costs due to soil erosion, loss of fertility, and the need to invest in climate-resilient infrastructure. These additional costs are passed on to prices, especially in agriculture, where yields decline due to climate variability, reducing local supply. The weakness of national production forces Gabon to rely more on imports, exposing the economy to international price fluctuations and rising logistical costs. Infrastructure, already vulnerable, deteriorates rapidly in the face of extreme climate events, leading to significant public expenditures for maintenance or modernization. These additional costs often result in tax hikes or increased public service fees, indirectly fueling inflation.

Moreover, the decline in overall productivity due to crop losses, logistical disruptions, and health impacts reduces the economy's ability to meet growing demand, exacerbating price pressures. At the same time, the government's increasing debt to finance climate adaptation could lead to monetary inflation if the debt is monetized. A potential decline in oil revenues, caused by international climate restrictions or infrastructure shocks, would further weaken public finances, limiting the state's ability to stabilize prices. Inflation expectations also play a key role: households and businesses, perceiving persistent instability, adjust their behavior by increasing wage demands and prices, fueling a vicious cycle. Finally, the depletion of essential natural resources, such as forests and oil, reduces Gabon's capacity to sustain balanced economic growth, increasing extraction, processing, and distribution costs. Thus, climate change creates long-term structural inflation in Gabon by combining cost pressures, increased import dependency, and self-reinforcing macroeconomic imbalances.

Figure 4. Summary of the long-term inflationary effects channel.

6. Recommendations

Although Gabon cannot directly influence global decisions on environmental protection, pollution control, the arms race, or methane emissions, we propose that it focus on policies aimed at mitigating the impact of climate change on local price volatility. To achieve this, several actions can be considered:

1. Diversification of the economy to reduce dependence on natural resources and external factors.

2. Industrialization to strengthen local processing of raw materials and create added value.

3. Improvement of transport infrastructure (roads, railways, ports, etc.) to optimize supply chains and reduce logistical costs.

4. Implementation of an effective Corporate Social Responsibility (CSR) policy to integrate environmental and social issues into economic development.

5. Strict application of the 'polluter pays' principle to hold economic actors accountable for the negative externalities of their activities.

6. Acceleration of integration into the carbon credit market, allowing the monetization of efforts to reduce greenhouse gas emissions.

7. Conclusion

In conclusion, this study examines the relationship between global temperature changes and the monetary well-being of Gabonese households, analyzed through the Consumer Price Index (CPI). The results, obtained via an ARDL estimation capturing temporal dynamics, show that a one-unit increase in temperature could, in the long term, lead to a rise of more than 94 points in the CPI. Such a development would significantly deteriorate the monetary well-being of households.

In the short term, a correction effect has been observed. A rise in temperatures immediately leads to an increase in inflation. However, after an adjustment period where inflation is accounted for, deflationary trends emerge. This phenomenon could be explained by several factors, including the implementation of policies aimed at combating high living costs, such as the establishment of price regulations, as well as the inherent instability of climatic phenomena.

However, we acknowledge certain limitations in our work, particularly regarding the sample size, which is at the threshold of acceptability, as well as the specification of the estimation. While the latter is generally correct, as evidenced by the analysis of error variations, some additional variables could have been considered to refine the results.

Abbreviations

ARDL | Auto-Regressive Distributed Lag |

CPI | Consumer Price Index |

CSR | Corporate Social Responsibility |

CUSUM | Cumulative Sum Test |

CUSUMSQ | Cumulative Sum of Squares Test |

ECT | Error Correction Term |

GDP/H | Gross Domestic Product per Capita |

LM | Lagrange Multiplier |

OLS | Ordinary Least Squares OLS) |

p-value | Probability Value |

Conflict of Interest

The authors declare no conflicts of interest.

References

| [1] |

Alla, Semenova. (2023). 2. Rising temperatures and rising prices: the inflationary impacts of climate change and the need for degrowth-based solutions to the ecological crisis. Globalizations,

https://doi.org/10.1080/14747731.2023.2222482

|

| [2] |

Amar, Rao., Brian, Lucey., Satish, Kumar. (2023). 1. Climate risk and carbon emissions: Examining their impact on key energy markets through asymmetric spillovers. Energy Economics,

https://doi.org/10.1016/j.eneco.2023.106970

|

| [3] |

Batten, S., Sowerbutts, R. et Tanaka, M. (2020). Changement climatique: impact macroéconomique et implications pour la politique monétaire. Les risques écologiques, sociétaux et technologiques et le secteur financier, 13-38.

|

| [4] |

Burke, M., Hsiang, S. M. et Miguel, E. (2015). Effet non linéaire global de la température sur la production économique. Nature, 527(7577), 235-239.

|

| [5] |

Dell, M., Jones, B. F., & Olken, B. A. (2012). Temperature shocks and economic growth: Evidence from the last half century. American Economic Journal: Macroeconomics, 4(3), 66-95.

|

| [6] |

Fonds Monétaire International (FMI) (2021). World Economic Outlook: Managing Divergent Recoveries. FMI Publications.

|

| [7] |

Hyacinth, E., Ichoku., Ihuoma, Anthony., Tosin, Olushola., Apinran, Martins. (2023). 5. Modelling Dynamic Linkage between Climate Change and Food Inflation in Nigeria. International Journal of Enviornment and Climate Change,

https://doi.org/10.9734/ijecc/2023/v13i113272

|

| [8] |

Maximilian, Kotz., Friderike, Kuik., Eliza, Lis., Christiane, Nickel. (2024). 1. Global warming and heat extremes to enhance inflationary pressures.

https://doi.org/10.1038/s43247-023-01173-x

|

| [9] |

Maximilian, Kotz., Friderike, Kuik., Eliza, Lis., Christiane, Nickel. (2023). 2. The Impact of Global Warming on Inflation: Averages, Seasonality and Extremes. Social Science Research Network,

https://doi.org/10.2139/ssrn.4457821

|

| [10] |

Mohammed, M., Tumala., Afees, A., Salisu., Yaaba, Baba, Nmadu. (2023). 5. Climate change and fossil fuel prices: A GARCH-MIDAS analysis. Energy Economics,

https://doi.org/10.1016/j.eneco.2023.106792

|

| [11] |

Paul, Chinowsky., Carolyn, Hayles., Amy, Schweikert., Niko, Strzepek., Kenneth, Strzepek., C., Adam, Schlosser. (2011). 1. Climate change: comparative impact on developing and developed countries.

https://doi.org/10.1080/21573727.2010.549608

|

| [12] |

Ramesh, Allipour, Birgani., Ali, Kianirad., Sakineh, Shab-Bidar., Abolghasem, Djazayeri., Hamed, Pouraram., Amirhossein, Takian. (2022). 4. Climate Change and Food Price: A Systematic Review and Meta-Analysis of Observational Studies, 1990-2021. American Journal of Climate Change,

https://doi.org/10.4236/ajcc.2022.112006

|

| [13] |

RFI. (2022, 27 décembre). Gabon: Tous les trains bloqués après un éboulement sur le Transgabonais. Consulté le 16 décembre 2024, à l’adresse

https://www.rfi.fr/fr/afrique/20221227-gabon-tous-les-trains-bloqu%C3%A9s-apr%C3%A8s-un-%C3%A9boulement-sur-le-transgabonais

|

| [14] |

Stern, N., et Taylor, C. (2007). Changement climatique: risque, éthique et la revue Stern. Science, 317 (5835), 203-204.

|

| [15] |

Yang, X., Xiong, J., Du, T., Ju, X., Gan, Y., Li, S.,... & Butterbach-Bahl, K. (2024). La diversification de la rotation des cultures augmente la production alimentaire, réduit les émissions nettes de gaz à effet de serre et améliore la santé des sols. Nature Communications, 15 (1), 198.

|

| [16] |

Khan, Z., Badeeb, RA, et Nawaz, K. (2022). Ressources naturelles et performance économique: évaluation du rôle du risque politique et de la consommation d’énergies renouvelables. Politique des ressources, 78, 102890.

|

| [17] |

Birgani, RA, Kianirad, A., Shab-Bidar, S., Djazayeri, A., Pouraram, H., et Takian, A. (2022). Changement climatique et prix des denrées alimentaires: revue systématique et méta-analyse d’études observationnelles, 1990-2021. American Journal of Climate Change, 11 (2), 103-132.

|

Cite This Article

-

ACS Style

Ndong, S. P. N.; Digossou, E. L.; Oumarou, M. M.; Ondo, M. E. N. The Impact of Global Temperatures on Inflation in Gabon. Int. J. Finance Bank. Res. 2025, 11(3), 46-55. doi: 10.11648/j.ijfbr.20251103.11

Copy

|

Copy

|

Download

Download

-

@article{10.11648/j.ijfbr.20251103.11,

author = {Streley Paul N’Nang Ndong and Elfi Lionnel Digossou and Mohamed Metoulou Oumarou and Marc Edgard Ndong Ondo},

title = {The Impact of Global Temperatures on Inflation in Gabon

},

journal = {International Journal of Finance and Banking Research},

volume = {11},

number = {3},

pages = {46-55},

doi = {10.11648/j.ijfbr.20251103.11},

url = {https://doi.org/10.11648/j.ijfbr.20251103.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijfbr.20251103.11},

abstract = {This article analyzes in depth the impact of global temperature variations on inflation in Gabon through the application of an Autoregressive Distributed Lag (ARDL) model. The analysis is based on annual data covering the period 1990–2023, which makes it possible to capture both the short- and long-term dynamics between climate shocks and price fluctuations. The central objective is to understand how climate anomalies, particularly temperature increases, translate into macroeconomic instability in a country that is highly dependent on imports and whose infrastructure remains vulnerable to external shocks. The results show that a one-degree Celsius rise in average global temperature compared to the 20th-century baseline leads to a long-term increase of approximately 94 points in the Consumer Price Index (CPI). This reflects not only higher prices for essential goods but also a deterioration in the monetary well-being of households, especially the most fragile groups. In the short run, climate shocks tend to generate immediate inflationary pressures, often followed by temporary deflationary episodes as markets attempt to adjust. These fluctuations are amplified by structural weaknesses, such as heavy reliance on imported food products, limited diversification of the economy, and insufficient resilience of transport and energy systems. By integrating climate dynamics into inflation analysis, this study fills a gap in the African economic literature, where environmental variables are still rarely included in macroeconomic models. The findings provide useful insights for policymakers by emphasizing the urgent need for climate adaptation strategies, economic diversification, and stronger social protection systems. In doing so, the paper contributes to the broader debate on the links between climate change, price stability, and sustainable development in Sub-Saharan Africa, using Gabon as a case study.

},

year = {2025}

}

Copy

|

Download

-

TY - JOUR

T1 - The Impact of Global Temperatures on Inflation in Gabon

AU - Streley Paul N’Nang Ndong

AU - Elfi Lionnel Digossou

AU - Mohamed Metoulou Oumarou

AU - Marc Edgard Ndong Ondo

Y1 - 2025/08/29

PY - 2025

N1 - https://doi.org/10.11648/j.ijfbr.20251103.11

DO - 10.11648/j.ijfbr.20251103.11

T2 - International Journal of Finance and Banking Research

JF - International Journal of Finance and Banking Research

JO - International Journal of Finance and Banking Research

SP - 46

EP - 55

PB - Science Publishing Group

SN - 2472-2278

UR - https://doi.org/10.11648/j.ijfbr.20251103.11

AB - This article analyzes in depth the impact of global temperature variations on inflation in Gabon through the application of an Autoregressive Distributed Lag (ARDL) model. The analysis is based on annual data covering the period 1990–2023, which makes it possible to capture both the short- and long-term dynamics between climate shocks and price fluctuations. The central objective is to understand how climate anomalies, particularly temperature increases, translate into macroeconomic instability in a country that is highly dependent on imports and whose infrastructure remains vulnerable to external shocks. The results show that a one-degree Celsius rise in average global temperature compared to the 20th-century baseline leads to a long-term increase of approximately 94 points in the Consumer Price Index (CPI). This reflects not only higher prices for essential goods but also a deterioration in the monetary well-being of households, especially the most fragile groups. In the short run, climate shocks tend to generate immediate inflationary pressures, often followed by temporary deflationary episodes as markets attempt to adjust. These fluctuations are amplified by structural weaknesses, such as heavy reliance on imported food products, limited diversification of the economy, and insufficient resilience of transport and energy systems. By integrating climate dynamics into inflation analysis, this study fills a gap in the African economic literature, where environmental variables are still rarely included in macroeconomic models. The findings provide useful insights for policymakers by emphasizing the urgent need for climate adaptation strategies, economic diversification, and stronger social protection systems. In doing so, the paper contributes to the broader debate on the links between climate change, price stability, and sustainable development in Sub-Saharan Africa, using Gabon as a case study.

VL - 11

IS - 3

ER -

Copy

|

Download